Madisonville, Fairfax, and Newport: Where Cincinnati Investors Are Finding Margin in 2026

Madisonville, Fairfax, and Newport: Where Cincinnati Investors Are Finding Margin in 2026

By Slocomb Reed & Ian Cruz, CPA | The Cincy REI Show

A veteran Cincinnati realtor and investor breaks down which neighborhoods are still producing deals in 2026, where margins have compressed, and why Northern Kentucky is drawing serious attention from Ohio-side flippers.

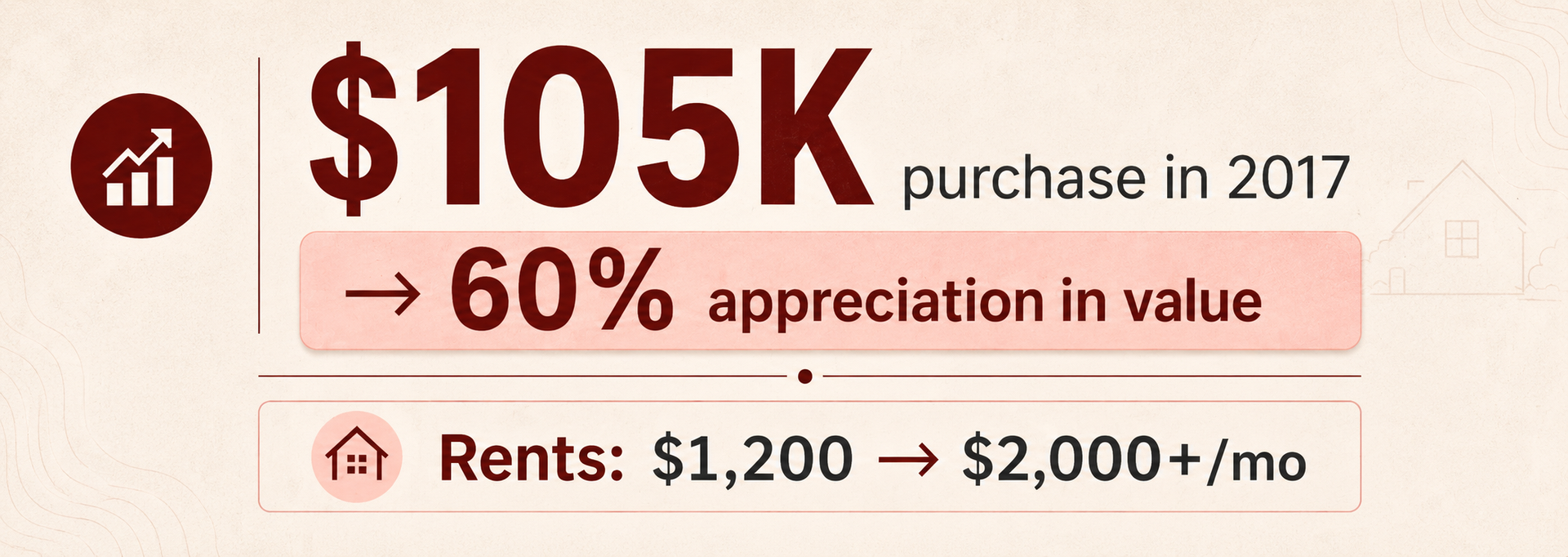

A Madisonville buy-and-hold purchased for $105,000 in 2017 with a $1,200 rent target now commands $2,000 or more per month, and the underlying asset has appreciated roughly 60% in value. That is the before-and-after summary of Cincinnati's most investor-active neighborhood over the past decade. The Cincy REI Show, hosted by Slocomb Reed and Ian Cruz, CPA, dug into that trajectory with a longtime local investor and realtor who has owned rental property in Madisonville long enough to watch a major mixed-use corridor get built on Madison Road while he still held houses on nearby streets.

Madisonville, Fairfax, and Newport: Which Neighborhoods Are Still Producing in 2026

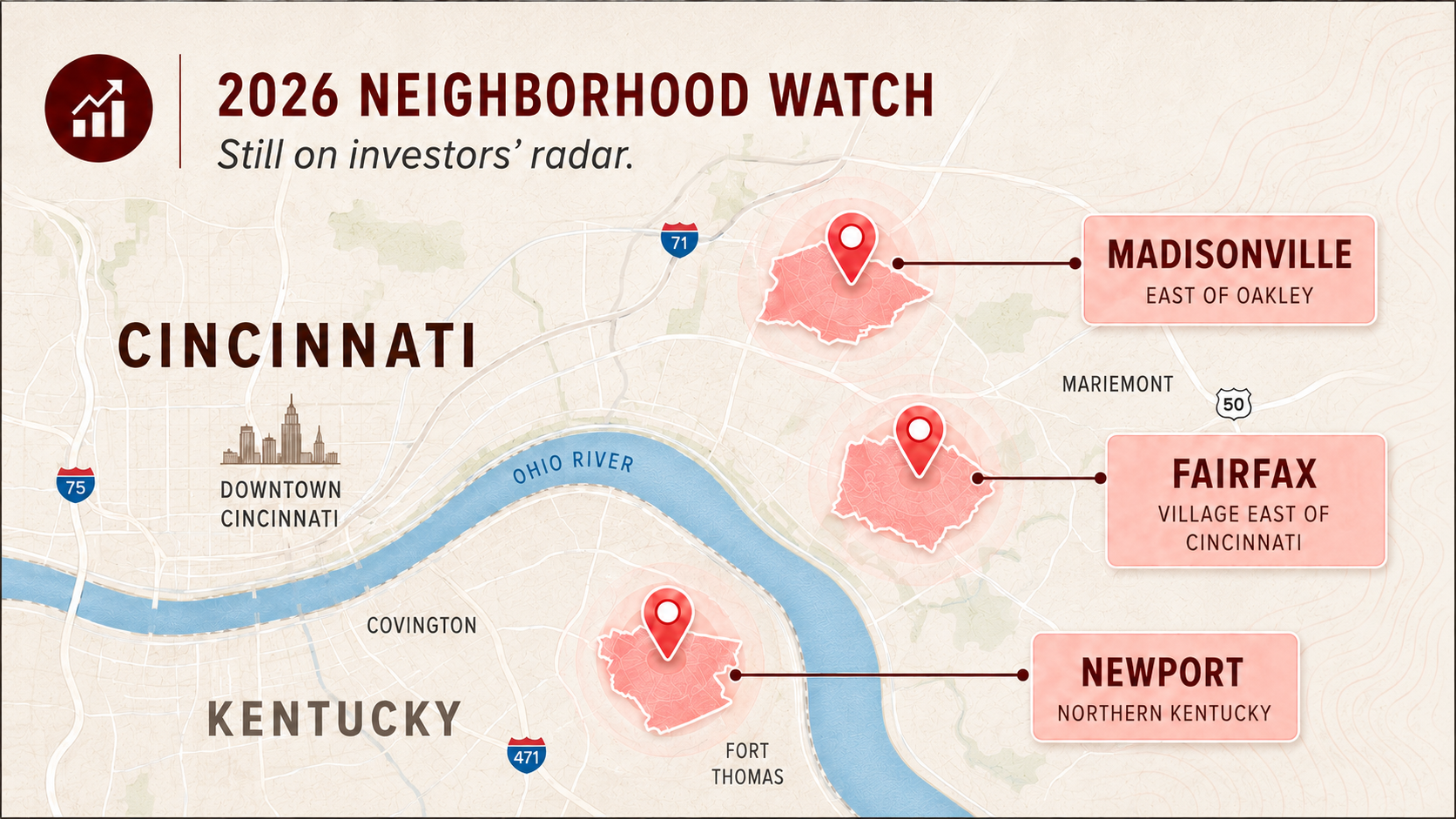

The three neighborhoods that dominated this conversation each represent a different stage of the Cincinnati investor lifecycle: one that has repriced and narrowed, one that has gentrified and shifted to new construction, and one across the river that is drawing attention specifically because of lower carrying costs.

Madisonville has been the most investor-transformed neighborhood in Greater Cincinnati over the past decade. In 2017, a knowledgeable buyer could acquire a solid housing stock property for under $100,000, rent it at $1,200, and face minimal competition. That playbook has compressed significantly. Rents have moved to $2,000 and higher. Property values have followed. The investors and agents who drove that repricing are now the reason margins are thinner for new entrants. The opportunity that remains is in distressed situations: long-term homeowners who have been there 30 to 40 years and whose tax reassessments have made ownership unsustainable. These sellers are motivated and sometimes under-priced relative to current market. Value-add acquisitions with room to improve the asset and reposition rents remain viable, though the margin for error is narrower than it was in 2017.

Fairfax has followed a similar arc, but the strategy mix has shifted almost entirely toward new construction. The neighborhood sits west of Mariemont and benefits from the Mariemont school district, which has driven demand so aggressively that empty lots are selling for $120,000 to $150,000. The investor play that worked five to seven years ago, buying a two-bedroom, one-bath ranch, popping the top, and converting it to a four-bedroom, two-and-a-half bath, has largely run out of viable inventory. The current opportunity is lot acquisition for new construction. Builders who can source a lot around $120,000 are building three-bedroom, two-and-a-half bath homes with finished lower levels. Lot geometry in Fairfax tends to run narrow, which is pushing some builders toward townhouse-style layouts: garage and entry at grade, main living on the second floor, bedrooms above. That format is meeting buyer demand in a neighborhood where lot widths do not support traditional footprints.

Newport, Kentucky is the emerging flip market for Ohio-based investors who have been priced out of their home turf. Property taxes run lower than Hamilton County even accounting for the double-tax structure (city plus county). The cost of ownership is meaningfully lower. The trade-off is a steeper operational learning curve. Newport's building department runs strict inspections and maintains close oversight of contractor licensing. Ohio-licensed contractors who have not established a Kentucky license will be flagged. The practical implication: expect an expensive first rehab in Newport while you build your contractor network. Once those relationships are established, the economics sharpen significantly.

Evanston and the west side of Cincinnati also surfaced as neighborhoods where deal flow still exists. They were described as directional signals rather than fully developed plays, but both were named as areas worth monitoring for investors who have been crowded out of Madisonville.

Rising Rates, Higher Taxes, and Better Information Have Compressed Cincinnati Margins

The structural shift in Greater Cincinnati real estate over the past five years comes down to three compounding pressures.

- Interest rates moved from 3% to 6%. Every underwrite that worked at 3% has to be rebuilt from scratch at 6%. Deals that produced solid cash-on-cash returns under the old rate environment require either a lower acquisition price, a higher rent ceiling, or both. The deals that still work are the ones where the basis is low enough that the carry cost does not kill the return.

- Property tax reassessments have reset the operating cost baseline. This is a particularly acute issue in Madisonville, where decades-long homeowners are now carrying tax bills that make continued ownership difficult. That is a pain point for sellers and an opportunity for buyers, but it also means that any buy-and-hold underwrite in appreciating Cincinnati neighborhoods needs to stress-test taxes at the current assessed value, not prior-year basis.

- Information availability has equalized the buyer pool. A decade ago, Cincinnati's most productive investor neighborhoods were effectively word-of-mouth markets. Agents covered their research. Investors operated quietly. That era is over. BiggerPockets, Zillow, and broader investor education have brought more capital into every neighborhood that was once underfollowed. Madisonville's repricing from the mid-$80,000s to current values is partly a function of that information democratization. The investors who got rich in Madisonville got in before the neighborhood was indexed. That window has closed.

“The investors who got rich in Madisonville got in before the neighborhood was indexed. That window has closed.”

The directional read from an operator who has watched this cycle from inside: the next wave of Cincinnati deals will come from neighborhoods adjacent to gentrified corridors, distressed sellers in recently repriced markets, and cross-river opportunities in Northern Kentucky where the tax and cost structure still offers room.

What's Working in Cincinnati

| Strategy | Best-Fit Markets | Key Underwriting Focus |

|---|---|---|

| Buy-and-hold rental | Madisonville (distressed/off-market), Evanston, west side pockets | Rent-to-basis ratio, tax reassessment exposure, property management quality, long-term tenant demand |

| Fix-and-flip | Newport, Covington, select Cincinnati pockets with resale demand | Acquisition basis, contractor licensing (KY), inspector relationship, holding costs, comps |

| New construction | Fairfax, infill lots near strong school district demand | Lot basis ($120K target or below), build cost, floor plan demand, townhouse vs. conventional layout |

| Value-add repositioning | Madisonville (motivated sellers, tax-stressed homeowners) | Below-market acquisition, clear improvement path, rent upside relative to current market |

A few principles that are consistently separating productive Cincinnati investors from those who are spinning their wheels:

- Geographic concentration compounds. An investor who focuses on five to ten properties in a single neighborhood builds deal flow faster than one who scatters. Sellers talk to neighbors. Contractors know the block. An investor who is consistently present in a neighborhood hears about opportunities before they hit Zillow.

- The margin is the filter. Deals in every Cincinnati neighborhood get evaluated the same way: does the margin work at current purchase price, current rates, and current operating costs? If yes, move forward. If the margin is thin, the deal requires a specific catalyst (rent growth, forced appreciation, cost reduction) that has to be clearly identified before closing, not assumed.

- Contractor access determines flip economics. In Newport specifically, going in without an established Kentucky-licensed contractor network means absorbing the learning curve cost on the first deal. That cost is real. Investors who have built those relationships are running better numbers on subsequent deals.

What does not work: entering any Greater Cincinnati neighborhood with an assumption that appreciation will bail out a deal with weak fundamentals at acquisition. The appreciation era in Madisonville rewarded everyone who owned. The next cycle will be more selective.

Lessons From the Field: How Margin Discipline Prevented a Second 2008

The investor who joined this episode came up the hard way. His first partnership worked well until it did not. In 2005, he teamed with a capital partner on a simple arrangement: find the deals, run the rehabs, the partner handles the financing. It grew. It accelerated. And it was under-capitalized the entire time.

When 2008 arrived, the model collapsed. The capital partner, a salaried employee with a stable income, made the decision to stop funding. He came in person to deliver the news. The portfolio had to be liquidated quickly. In a recession. Without the option of bankruptcy. The credit score took the hit. The path out was grinding through property sales one by one, keeping his word to every counterparty who gave him an extra day, and eventually coming out the other side with his reputation intact even if his balance sheet was not.

The recovery took years and a significant shift in risk tolerance. He spent roughly five years as a risk-averse operator, slowly re-entering the market. When he did come back, he came back smaller, more disciplined, and with a different framework. Single family. Concentrated geography. Margin as the first filter, not the last.

The outcome, held Madisonville properties bought in 2017 at under $105,000 have appreciated approximately 60% in value. Rents on those same houses have moved from a $1,200 target to $2,000 and above.

Four takeaways that apply to any Cincinnati investor entering the market now:

- Capitalization is a prerequisite, not a variable. A deal that requires a partner's capital to remain stable is only as solid as that relationship. Stress-test the capital structure before closing anything.

- Geographic focus accelerates deal flow. Concentrated ownership in one neighborhood creates organic opportunities: neighbors who know you, off-market conversations that come to you because you are visible and consistent.

- Know your numbers before you know your neighborhood. Margin first, location second. An attractive neighborhood with a deal that does not pencil is still a deal that does not pencil.

- The first deal does not have to be a home run. The goal of the first acquisition is to complete the learning cycle, evaluate whether the asset class fits your operating style, and preserve the option to do a second one. Buying right gives you an exit if the answer is no.

Final Takeaway

Greater Cincinnati is not a uniform market, and 2026 is not 2017. The neighborhoods that made early investors wealthy have repriced. The margins that made buy-and-hold obvious have narrowed. The operators who are still finding deals are doing it through geographic discipline, cost structure awareness, and willingness to look at markets that are one step removed from the obvious ones: Northern Kentucky, Evanston, the west side.

If you are evaluating Cincinnati real estate investing right now, the most useful thing you can take from this episode is a framework that has survived two market cycles: define your margin before you pick your market, concentrate your operations, and build relationships that bring you deals before they are widely visible.

🎧 Subscribe to the Cincy REI Show on Spotify, Apple Podcasts, or YouTube to follow neighborhood-level analysis from local operators who are active in the market.